BYU Student Author: @Alex_Garrett

Reviewers: @Boston, @Nate, @Spencer

Estimated Time to Solve: 15 Minutes

We provide the solution to this challenge using:

- Excel

Need a program? Click here.

Overview

You have been working as an auditor in Southern California for the past 2 years now, and you are having a blast! One of the clients you are currently working on is Cowabunga Surf, a small company based in San Diego that purchases and resells the latest and greatest surfboards. They promised that at the end of the audit, you can take home a surfboard of your choice, so you want to do an excellent job.

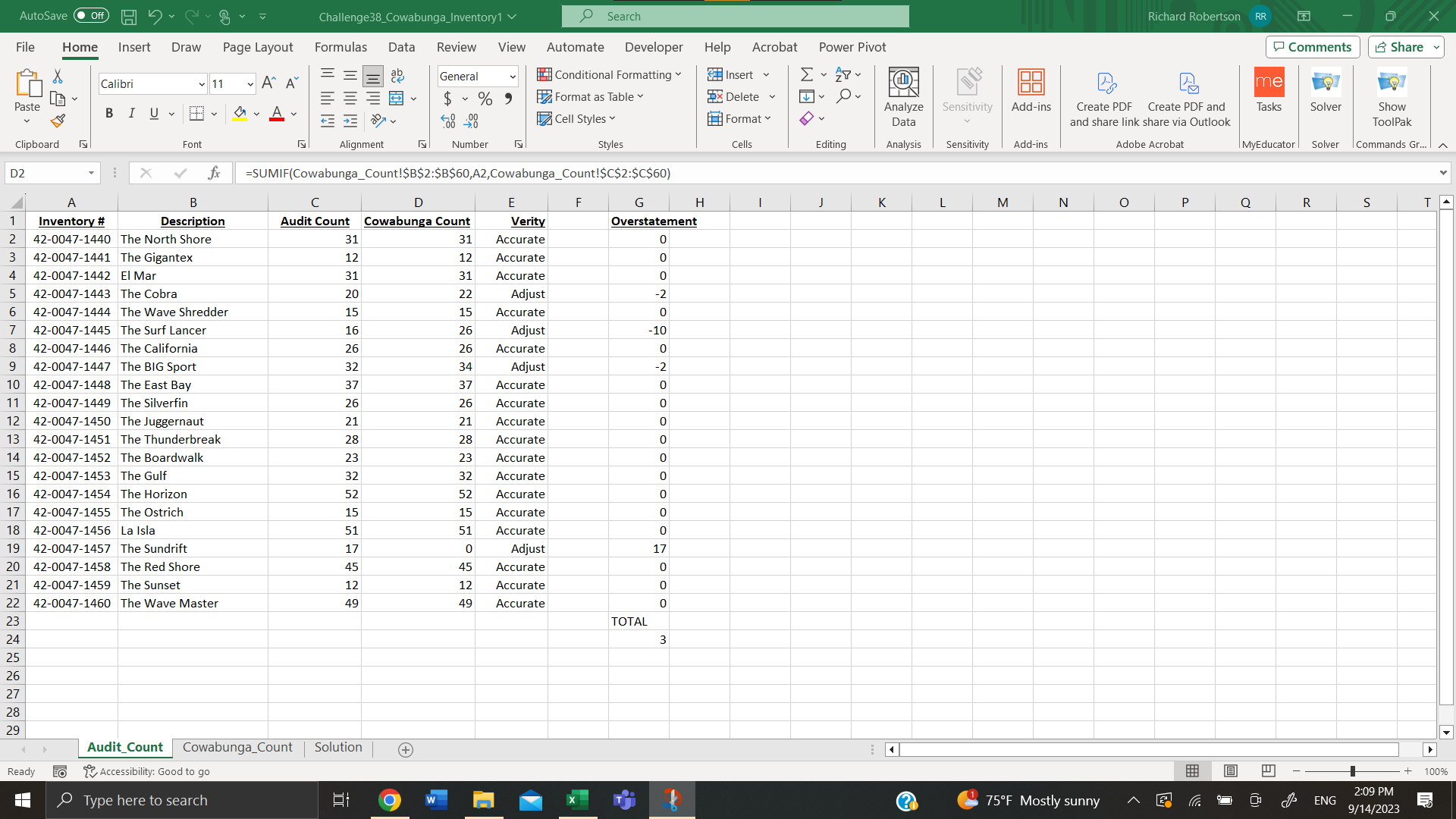

It’s now January 1st, and you are counting inventory and matching your count against the company’s count. Cowabunga Surf has a higher-than-average inventory turnover (i.e., they sell their inventory quickly). As a result, there isn’t a lot to count, so you decide to count every individual surfboard. Your findings are on the “Audit_Count” sub-sheet in the “Cowabunga_Inventory” spreadsheet. The company has also provided the inventory count that they have on record as of January 1st on the “Cowabunga_Count” sub-sheet in the same spreadsheet mentioned above. This sheet, however, did not include the following tags that were found by the company after it had already submitted its count. Make sure to update Cowabunga’s inventory count with the following additional tag numbers before starting your analysis. NOTE: For best results, enter the data manually as Excel’s auto-formatting may mess up further analysis.

- Tag #4019, Inventory #42-0047-1453, Quantity: 6, Plant: CA99

- Tag #8068, Inventory #42-0047-1443, Quantity: 2, Plant: WA13

- Tag #4020, Inventory #42-0047-1447, Quantity: 1, Plant: CA99

- Tag #4021, Inventory #42-0047-1453, Quantity: 3, Plant: CA99

Instructions

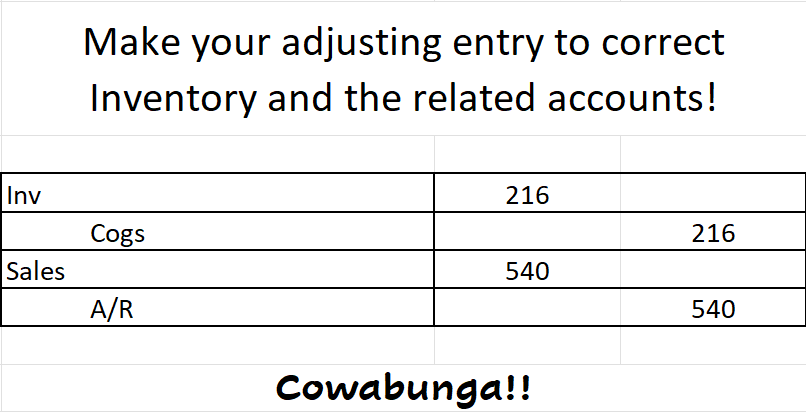

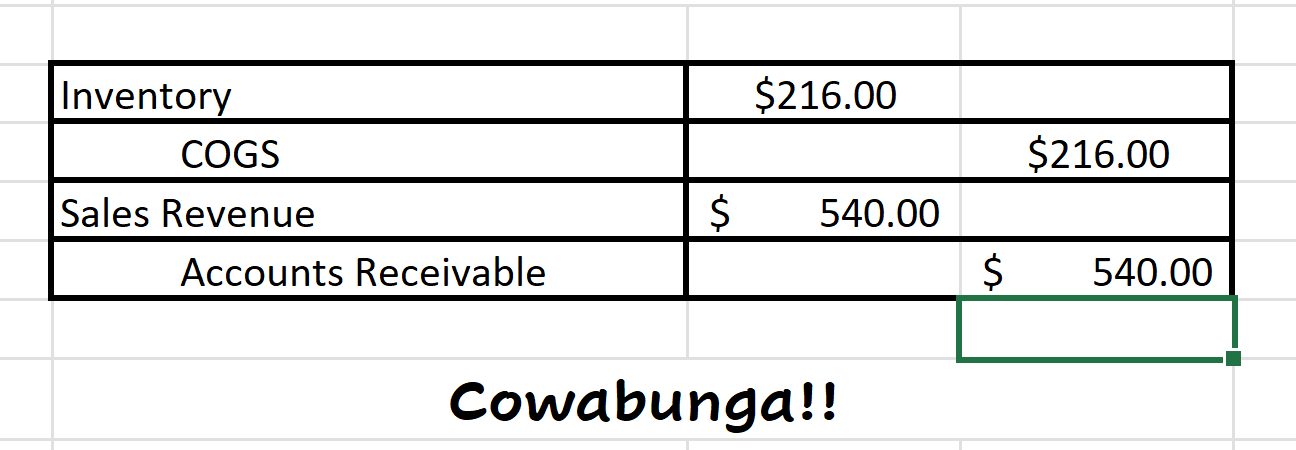

Your job is to compare your inventory count with the count provided by Cowabunga Surf. For purposes of this challenge, assume that your count (the auditor) is correct and that inventory needs to be adjusted to reflect the correct number. Assume that the tolerable misstatement for the inventory account is 0 (i.e., we need to find all mistakes) and that any difference between your count and the company’s count is a mistake in sales. There are no timing differences. For example, if your count is higher than the company’s count, then sales are overstated. On the other hand, if your count is lower, sales are understated. At the end of the challenge, make an adjusting entry to reflect actual inventory and actual sales on the “Solution” sub-sheet. Assume that the books are still open for the year ended and that all sales are made on account.

Data Files

Suggestions and Hints

Look up how to use the subtotals feature in Excel to analyze the data quickly. The SUMIF() function can also be used to summarize the data.

Solution

Challenge38_Solution.xlsx

Solution Video: Challenge 38|EXCEL – Cowabunga Surf Audit